The spreadsheet landed in my inbox two days before close. A retention bonus plan covering 200 people, roughly 20% of the acquired workforce. Every VP got 50%. Every director got 30%. A few “critical” individual contributors got 25%. Total cost: $18M. The rationale was a single sentence: “Retention is critical to integration success.”

Nobody had asked which of those 200 people were actually at risk of leaving. Nobody had assessed which roles were genuinely irreplaceable versus merely senior. The plan was a peanut butter spread, and the CFO approved it because the alternative felt worse.

Six months later, 85% of the bonused employees were still there. The program was declared a success. Slides were made. Backs were patted. But 85% of the non-bonused employees were also still there. The $18M had bought confidence, not retention. That’s an expensive placebo.

This is the retention bonus problem in M&A. The logic sounds right. The math usually doesn’t hold. And it’s one of the reasons the first 100 days of an integration matter so much: the retention decisions you make early define whether the deal economics hold.

The turnover problem is real

Start with what is true: acquired employees leave at alarming rates.

MIT Sloan found that acquired employees leave at 3x the baseline rate in Year 1. 34% versus 12% for regular hires. EY puts it higher for key employees: 47% in Year 1, 75% by Year 3. Mercer’s data (851 data points across 450 transactions) shows 40% of critical talent gone within 18-24 months.

These numbers are real. They represent product knowledge walking out the door, customer relationships moving to competitors, and institutional memory that no onboarding program can replace. It’s why retention is the HR integration workstream that most directly determines whether the deal economics hold.

The question isn’t whether retention matters. It’s whether throwing money at it works.

The ROI math nobody shows you

Here’s how the pitch usually goes.

A VP of Engineering makes $250K. Replacing her costs 2x salary, or $500K, once you factor in recruiting, ramp time, and lost productivity. A 50% retention bonus costs $125K. That’s a 4:1 return. Easy.

Except that math assumes she would have left without the bonus. She probably wouldn’t have. This is the part of the pitch that never gets a slide. MIT Sloan’s data says 66% of acquired employees stay through Year 1 without any bonus at all. WTW says bonused employees stay at about 80% through vesting.

The implied incremental retention from bonuses is roughly 14 percentage points. Not 80%. Not even close.

When you run probability-adjusted numbers on a broad program, the picture changes completely.

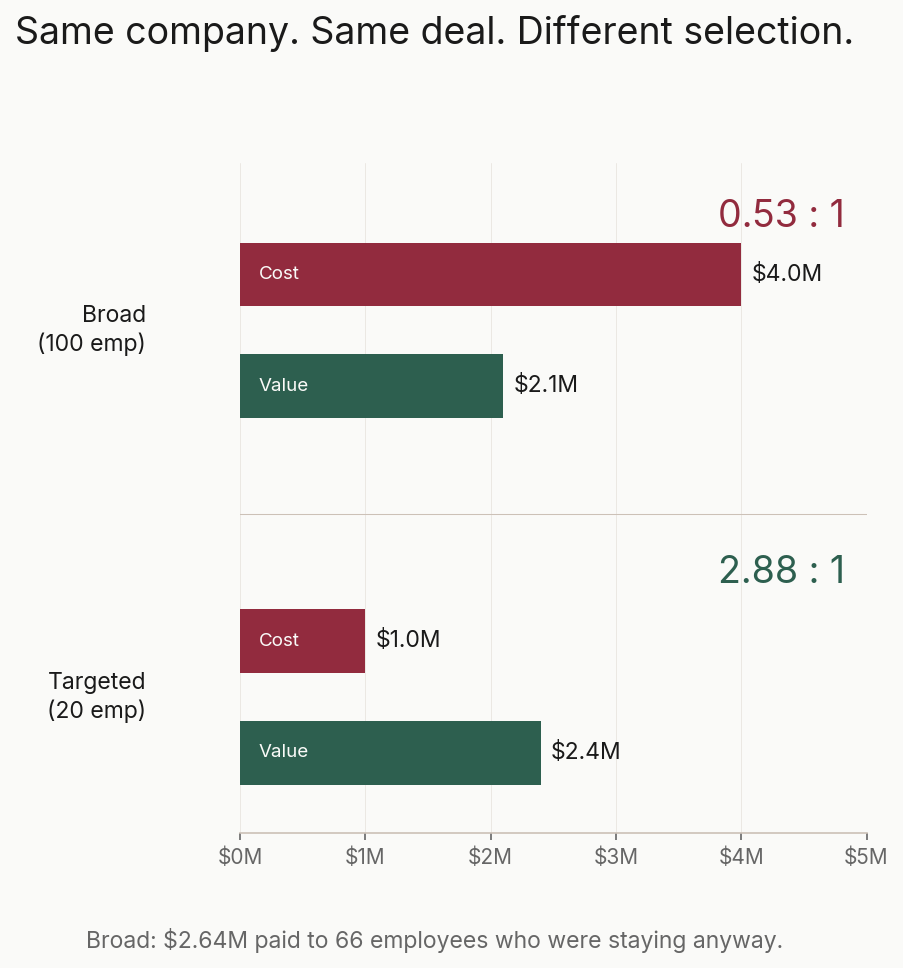

Take 100 employees, $100K average salary, 40% retention bonus:

- Without bonuses: 66 stay (MIT Sloan baseline)

- With bonuses: 80 stay (WTW data)

- Incremental saves: 14 employees

- Value of those 14 saves: 14 x $150K replacement cost = $2.1M

- Total bonus cost: 100 x $40K = $4.0M

- Deadweight (paid to the 66 who would have stayed anyway): $2.64M

- Adjusted ROI: $2.1M / $4.0M = 0.53:1

The program destroys value. For every dollar spent, you get 53 cents back.

Now run the same math on a narrow, targeted program. 20 employees, genuinely at risk (60% probability of leaving), genuinely critical (3x replacement cost), 50% bonus:

- Incremental saves: 20 x 0.40 (delta) = 8 employees

- Value of saves: 8 x $300K = $2.4M

- Total bonus cost: 20 x $50K = $1.0M

- Adjusted ROI: 2.88:1

Same company. Same deal. The only difference is who gets the bonus.

The break-even point for a broad program? The incremental retention delta would need to exceed 27 percentage points. No published data supports a delta that large.

The selection problem is everything

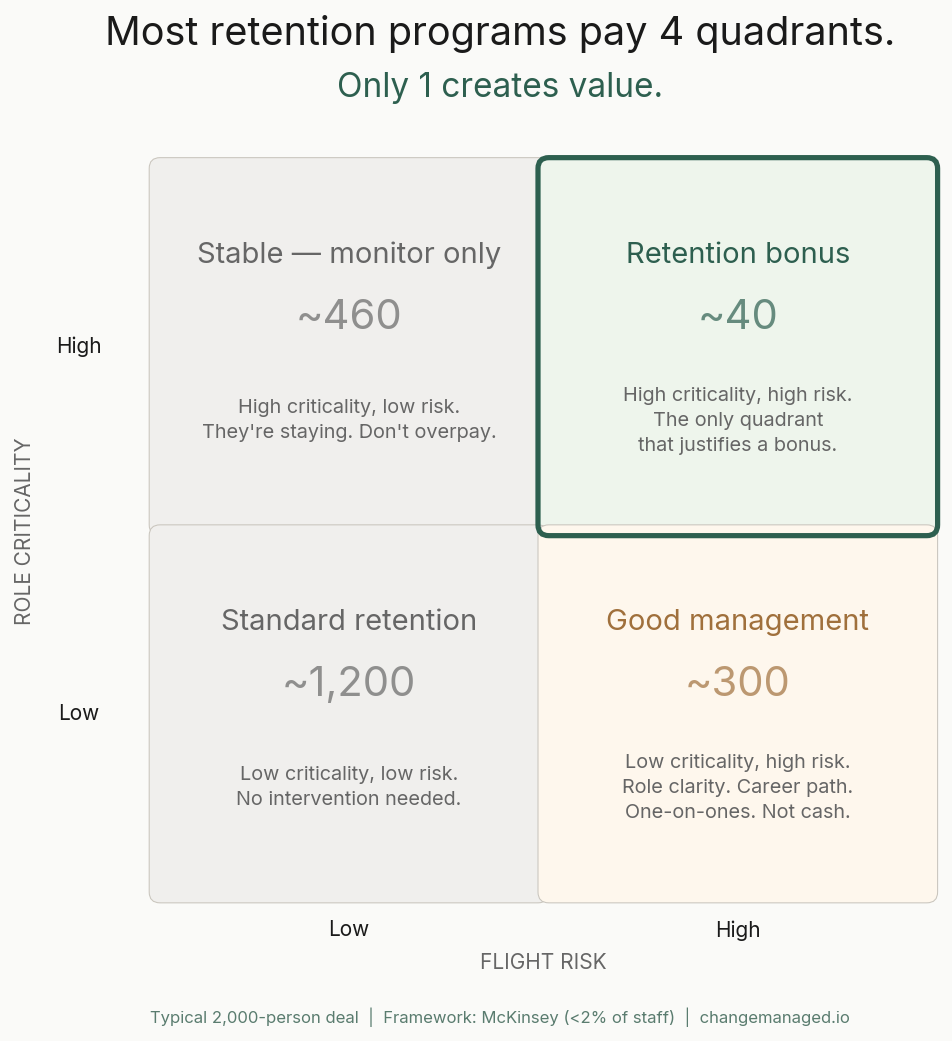

McKinsey’s research is clear on this: less than 2% of staff should receive retention incentives. About 40 transformation-critical roles create 80% of total value. Many of those roles aren’t senior leaders. They’re the mid-level specialists who know how the payroll custom logic works, or the regional sales director whose relationships generate $30M in annual revenue, or the IT architect who understands both legacy systems well enough to integrate them.

The selection problem comes down to four questions.

Is this role critical? If this person leaves, does revenue stop or do systems fail? Or can the work be redistributed? Most roles, even senior ones, fall into the second category.

Is this person actually at risk? LinkedIn activity. Competing offers. A career trajectory the combined org can’t match. Employees who are rooted, engaged, and loyal don’t need a bonus to stay. Paying them one is deadweight.

Is their knowledge concentrated? Sole owner of institutional knowledge that isn’t documented or transferable? That’s a different kind of risk than someone whose expertise is shared across a team.

Can you replace them? Four weeks to hire, or six months in a niche talent market? A $200K director in a commodity function is replaceable. A $150K specialist in a field with 200 qualified people globally is not.

Plot role criticality against flight risk on a 2x2. Only the high-criticality, high-flight-risk quadrant warrants a bonus. Everyone else gets good management, clear role clarity, and honest communication about their future. McKinsey’s data says those three things matter more than money anyway. A talent assessment that systematically evaluates both dimensions across the combined workforce is the starting point. Without it, you’re guessing.

Common mistakes

The most expensive one has a name: the peanut butter spread. Coverage should be roughly 5% of the workforce, not 20%. WTW’s 2024 data shows the median retention pool is 1-2% of purchase price. When you spread that across 20% of employees, each bonus is too small to change behavior and too expensive in aggregate.

Related: paying the loudest complainers instead of the quietest critical talent. The people who threaten to leave aren’t always the people you can’t afford to lose. Sometimes the specialist in the corner who never says a word is worth more than the VP who calls the recruiter every Monday.

Boards and steering committees default to retaining senior leaders, which creates a top-down bias. McKinsey found that the 40 most critical roles often include mid-level specialists. Directors who run day-to-day operations. Technical leads who hold the integration together. The “frozen middle” that gets overlooked in every retention discussion.

Then there’s the “all VPs get 50%, all directors get 30%” approach, which ignores the fact that one VP might be running a $500M P&L with no viable successor while another manages a function being consolidated. Same title, wildly different retention value.

One more: over-retention. Retaining people the combined org doesn’t need sends a confusing signal. If the synergy plan calls for a role elimination in 9 months, a 12-month retention bonus creates a problem, not a solution.

Structure and amounts

WTW’s 2024 study (159 respondents, 20+ countries) gives the clearest benchmark data.

| Level | WTW Median | Mercer Range |

|---|---|---|

| CEO / C-suite | 75-100% of base | 50-100% |

| Senior Leaders | 50% | 30-50% |

| Directors / Managers | 30% | 25-40% |

| Individual Contributors | 30% | 25-30% |

Four payment structures, each with trade-offs.

Lump sum is the most common. Single payment after the retention period. Clean, simple. But it creates a binary incentive: stay until the date, or don’t. Installments (50/50 at 6 and 12 months) reduce the cliff departure risk and maintain ongoing incentive, but add administrative complexity. Better for longer retention periods.

Milestone-based structures tie payment to integration achievements. Useful for integration-critical roles where you need the person AND their active engagement, not just their physical presence. Harder to define milestones that are fair and measurable. Hybrid (50% at close, 50% at milestone) balances immediacy with retention. The upfront payment signals commitment. The deferred payment signals that staying matters.

Budget benchmarks

- Median retention pool: 1-2% of purchase price (WTW 2024)

- 70% of companies keep pools below 2%

- Retention and transaction bonuses together represent 14% of total change-in-control benefits (Pearl Meyer, 1,200+ filings)

- 86% use cash for senior leaders; 56% supplement with RSUs

- Serial acquirers: 84% use pay-to-stay programs (Chief Executive/WTW)

The dry powder strategy

WTW recommends reserving 20-30% of the retention pool for deployment after close. The logic is sound. You don’t know who’s genuinely critical until you’re in the integration. The person running the TSA migration might not even be on your Day 1 retention list.

Award smaller initial grants. Hold back 20-30%. Deploy it at months 3-6 when you can see who’s actually indispensable. This is the single highest-ROI change most companies can make to their retention programs.

Timing

| Phase | What happens | Risk |

|---|---|---|

| Pre-announcement | Identify critical talent quietly. Build the framework. | Leaks create panic. |

| Announcement to close | Pre-close retention for deal-critical staff only. | Over-committing before knowing the combined org. |

| Day 1 (close) | Announce broader program. Deliver agreements within 1-2 weeks. | Delay beyond Week 2 sends the wrong signal. |

| Post-close (months 3-18) | Deploy dry powder to newly identified critical talent. | Too late for people already interviewing. |

The median retention period has shortened. WTW’s 2024 data shows 13-18 months, down from 2+ years in 2020. Fewer than 30% of programs now exceed 2 years. Deal timelines are also extending (now 14 months, up from 10 in 2020), which means companies need retention agreements ready earlier and for longer effective periods.

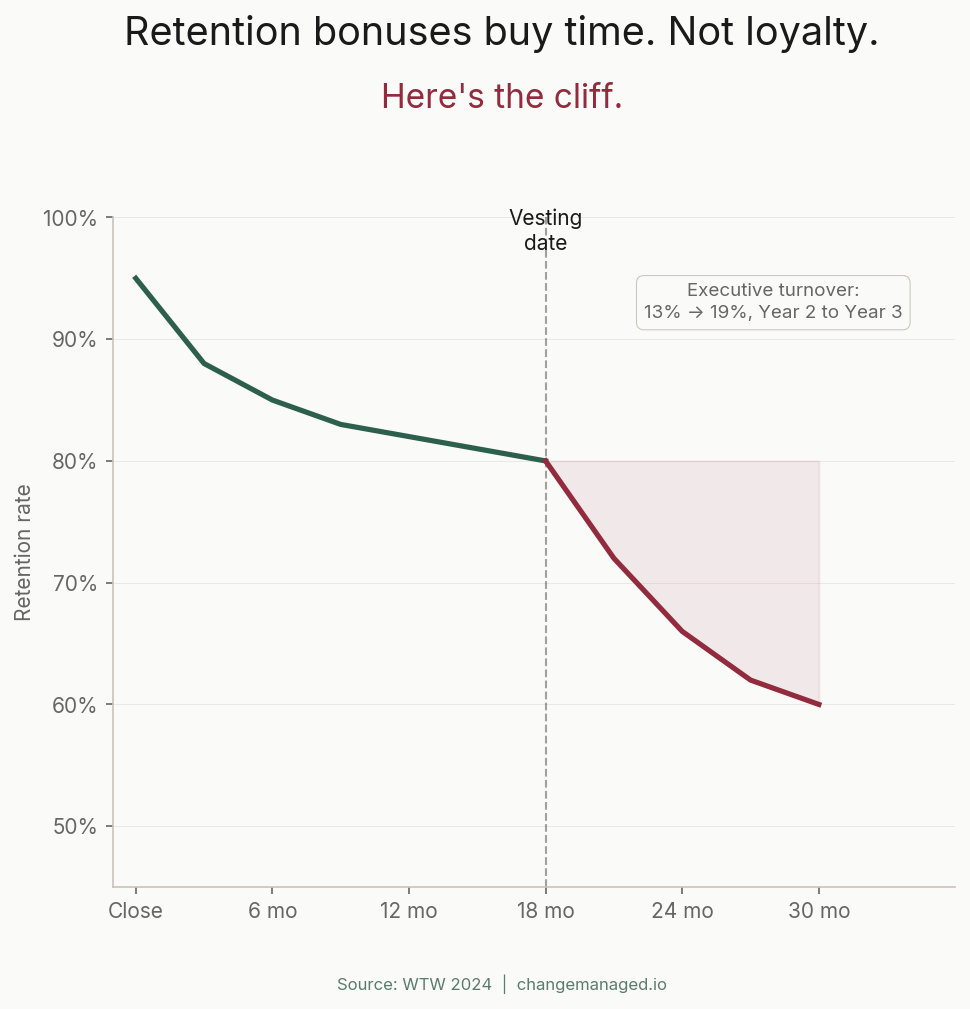

The cliff problem

Cliff-vested bonuses create a predictable departure wave. WTW data shows retention through vesting exceeds 80%. Post-vesting, it drops to roughly 60% within a year. Executive turnover spikes from 13% to 19% between Year 2 and Year 3. That 20-point drop is the strongest indirect evidence that bonuses buy time, not loyalty.

Mitigations: staggered grants, graded vesting, or transition to long-term incentives before the retention period expires. The integration team has the retained period to build engagement, career paths, and cultural belonging. If the only reason someone stays is the check, they’ll leave the day after it clears.

The international trap

Cross-border deals make retention programs more expensive and legally treacherous.

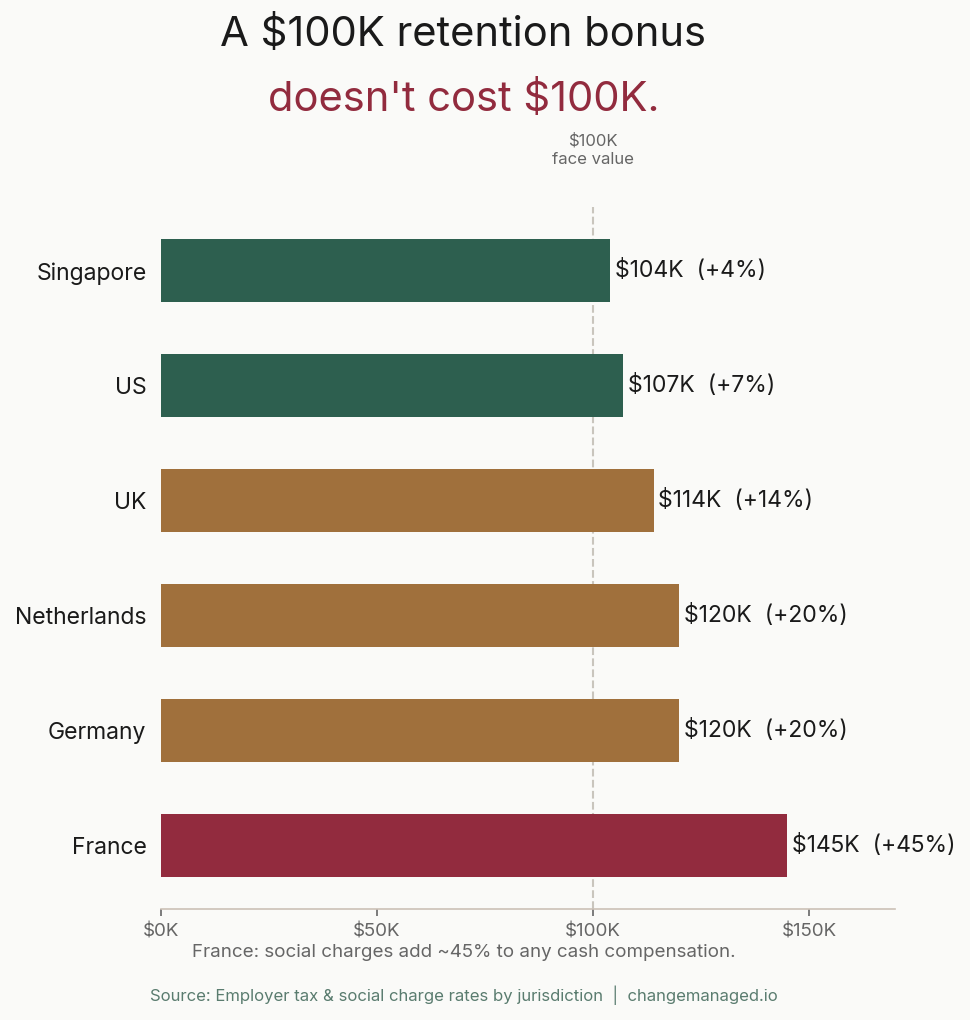

Employer-side costs

A $100K retention bonus doesn’t cost $100K in most countries.

| Country | Employer cost per $100K bonus |

|---|---|

| US | ~$107K (FICA) |

| Singapore | ~$104K (CPF) |

| UK | ~$114K (employer NIC) |

| Netherlands | ~$120K (social charges) |

| Germany | ~$120K (social + solidarity) |

| France | ~$145K (employer charges 25-42%) |

Budget 20-45% above face value for every European jurisdiction.

Clawback enforceability

This varies dramatically by country and changes the structural design of the program.

Generally enforceable: US, UK, Singapore, UAE. Deferred payment (pay after service) is cleaner than clawback (pay upfront, demand repayment), but both work.

Restricted: Germany (proportionality review by labor courts, excessive amounts struck down), Netherlands (employee can petition court to reduce “unfair” clawbacks), Australia (Fair Work Act protections).

Largely void: France (courts treat as penalty clauses), Brazil (CLT protects employee; bonus once paid is “acquired right”), Japan (Labor Standards Act limits deductions).

In civil law jurisdictions, use deferred payment structures. Structure retention bonuses as new, separate side agreements rather than variations to existing contracts. In carve-out transactions, this complexity multiplies because the employment relationship itself is transferring. If the bonus is linked to accepting new employment terms, it may be unenforceable under TUPE (UK/EU) where variations to transferred employee contracts are void if the principal reason is the transfer.

Works councils

In Germany and the Netherlands, works councils have co-determination rights over bonus schemes affecting employees. A retention program covering more than individual cases requires consultation before announcement. The Netherlands’ Ondernemingsraad (works council) can block changes to pay schemes entirely. A retention program covering more than 25% of staff qualifies as an “important decision” requiring formal advice.

Don’t announce your retention program in Germany before the works council has been consulted. It’s not a suggestion. It’s law.

Tax

Retention bonuses in the US are classified as supplemental wages. Flat federal withholding at 22% for the first $1M, 37% above that.

The bigger risk is Section 280G. Retention bonuses count toward “parachute payment” calculations. If an executive’s total change-in-control payments exceed 3x their base amount, a 20% excise tax applies to the excess. For senior leaders with multiple CIC benefits (acceleration, severance, retention), the 280G threshold can be triggered by the retention bonus alone.

Get tax counsel involved before finalizing amounts for anyone in the C-suite. The interaction between retention bonuses, equity acceleration, and severance is where 280G problems hide.

What actually works

The data on non-financial retention is stronger than most deal teams realize.

McKinsey surveyed 1,047 executives and found three non-cash motivators rated “no less or even more effective” than cash bonuses: praise from immediate manager, leadership attention (one-on-ones with senior leaders), and the chance to lead projects or task forces.

A separate McKinsey survey of 1,400 integration executives rated “praise from immediate manager” as the number one retention lever. Above bonuses. Above equity.

One European industrial case achieved 100% retention of targeted at-risk employees using only non-financial measures. Cost: 25% of the budget compared to cash programs.

This doesn’t mean you skip bonuses. It means bonuses are necessary but not sufficient. A $75K retention bonus paired with role ambiguity, no manager communication, and cultural dissonance will lose to a $25K bonus paired with a clear career narrative, regular one-on-ones, and a leadership team that visibly invests in the person’s future.

When WTW asked why employees leave despite receiving retention bonuses, the top reasons were cultural misalignment, strategic disagreement, and role dissatisfaction. Compensation was rarely cited.

Putting it together

The retention program that creates value looks nothing like the one most companies run.

Start narrow. 2-5% of the workforce, not 20%. Use the four-dimension framework to identify genuinely critical, genuinely at-risk roles. Hold back 20-30% of the pool as dry powder and deploy it at months 3-6 when you know who’s actually indispensable. McKinsey’s data says about 40 roles in a typical deal create 80% of the value. Find those 40.

Then pair money with management. Every bonused employee gets a career narrative from their direct manager within 30 days. Role clarity. Growth path in the combined org. Regular one-on-ones. The bonus buys time. The management retains.

For cross-border deals: deferred payment, not clawback. Consult works councils before announcing in Germany and the Netherlands. Budget 20-45% above face value for employer costs in Europe.

Watch the cliff. Stagger grants or transition to long-term incentives before the retention period ends. An 80% retention rate that drops to 60% the quarter after vesting is not a success. And measure incrementally. Track bonused versus non-bonused attrition in comparable populations. If both groups retain at 85%, the program is buying confidence, not retention. Real-time workforce tracking that shows retention rates by population makes this comparison possible. Over a third of companies don’t track retention rates at all (WTW). That’s how $18M programs get declared successful based on vibes.

The retention bonus market is a multi-billion-dollar annual expenditure with less empirical validation than most pharmaceutical placebos. Broad programs likely destroy value. Narrow, targeted programs for high-risk, high-value employees likely create it. The selection problem is everything. Get it right and the ROI is 3:1. Get it wrong and you’ve written $18M worth of checks to people who were staying anyway. For the complete integration checklist that puts retention in context with every other workstream, start there.

Related Reading

- HR Integration in M&A: The Playbook That Should Exist

- TSA Exit: Why Yours Will Take 18 Months (How to Cut It)

- How to Set Up an IMO That Actually Works

- Carve-Out Readiness: What to Build Before Day 1

If your retention program covers more than 5% of the workforce, the math probably doesn’t work. If you want help identifying which 2% actually matters, let’s talk.

Related Insights

Carve-Out Readiness Checklist: 23 Items Before Day 1

The priority-tiered carve-out checklist. What must work Day 1, what starts before close, and what can wait. HRIS, payroll, legal entities, compliance, ERP.

100-Day M&A Integration Plan

100-day post-merger integration plan: stabilize (0-30), execute (31-60), accelerate (61-100). Week-by-week milestones from real transactions.

Josh is a Roshco founder. 15+ years leading M&A integrations, org redesigns, and technology transformations across multiple multi-billion-dollar deals and carve-outs. Deloitte Human Capital alum. UPenn. Prosci certified. Navy veteran.

See it in action

Orgscout puts live deal intelligence behind the advisory work: dashboards, org design, and synergy tracking on real data.

Explore the platform