FIELD NOTES

TSA Exit: Why Yours Will Take 18 Months

The TSA was supposed to be 12 months. That’s what the deal model assumed. That’s what the board was told. Twelve months of transition services from the seller, then the carved-out entity would run independently.

It’s month 18. The seller’s IT team is building an invoice for the third extension. The pricing escalator kicked in two months ago. The CFO is doing math on a napkin, trying to figure out what this delay has cost in real dollars, and the number keeps getting bigger every time he adds a line.

This is not unusual. It’s the norm. If you’re reading this and your TSA is on schedule, congratulations. You’re in the minority. If you’re reading this and your TSA doesn’t exist yet, congratulations. You still have time to plan the exit before you sign the entrance.

PwC found that early TSA exit drives 5-7% value uplift. BCG calls separation costs “an especially heavy burden.” But nobody publishes the data on what companies actually negotiate, what the durations actually look like, or why almost every TSA runs longer than planned.

I pulled that data from SEC filings. Here’s what it shows.

What a TSA actually is

If you’ve never lived through one: a Transition Service Agreement is a contract where the seller keeps the lights on for the buyer after close. Payroll, benefits, IT, finance, facilities, procurement. Everything the carved-out entity used to get from the parent and can’t yet do on its own.

The seller charges cost-plus with a single-digit markup. Extensions trigger automatic fee escalators, typically 10% per month after the sunset date. Every month on the TSA is a month the buyer can’t fully integrate, transform, or optimize.

The incentive structure sounds clean. Seller wants to stop providing. Buyer wants to stop paying. In practice, the seller has limited motivation to help the buyer exit faster, and the buyer often doesn’t have the operational readiness to leave. So both sides sit in a TSA that neither wants but nobody is working hard enough to end. It’s a bad marriage where both parties could leave but the couch is comfortable.

What the data shows

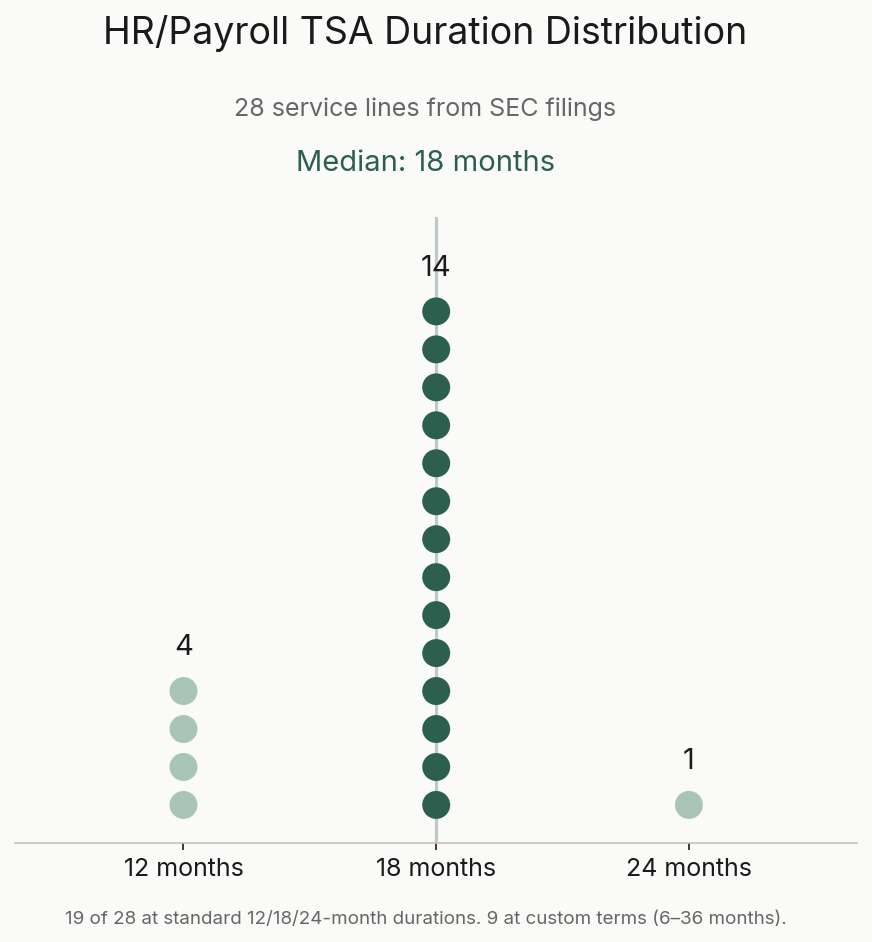

I analyzed publicly available SEC filing data across 36 deals and 250 service lines, including 28 specifically covering HR and payroll services. Real companies disclosing real TSA terms.

HR and payroll TSA durations

| Duration | Count | Examples |

|---|---|---|

| 12 months | 4 | BMS/Mead Johnson, Alkermes/Mural, Vista/Revelyst, Harley/LiveWire |

| 18 months | 14 | DuPont/Qnity, Kellanova/WK Kellogg, Danaher/Veralto, 3M/Solventum, GE/Vernova, BorgWarner/Phinia, LabCorp/Fortrea, NCR/Atleos, Zimmer/ZimVie, Western Digital/SanDisk, BD/Embecta, Fortive/Ralliant |

| 24 months | 1 | Comcast/Versant |

Median: 18 months. Companies negotiate 18 months because that’s how long it actually takes. The deals that negotiate 12 months tend to be simpler separations where the carved entity already has some standalone capability.

The cost of staying

BMS paid $152,580 per month for HR administration alone under its TSA with Mead Johnson. That’s one service line in one deal. Multiply across IT, finance, procurement, and facilities, and total TSA costs for a complex carve-out routinely hit seven figures per month.

PwC’s framework puts total value uplift from successful carve-outs at 8-11%, with 5-7% coming specifically from early TSA exit. On a $3B deal, that’s $150-210M in value left on the table by running long.

Why TSAs drag on

The most common reason is the simplest: nobody plans the exit. PwC estimates a typical TSA exit requires more than 1,500 interdependent design decisions. The legal team negotiates the service terms. The integration team focuses on integration. The exit? That’s a problem for later. Later becomes month 6, and month 6 becomes an extension request.

The second reason is vague service definitions. Over 40% of carve-out transactions involve TSA disagreements because the terms weren’t specific enough. When the TSA says “HR services” without specifying whether that includes benefits administration, HRIS access, talent management systems, and compliance reporting, every ambiguity becomes a negotiation. And these negotiations happen at exactly the moment you’re trying to separate, which is also the moment when the relationship between buyer and seller is at its most fraught. Great timing.

Then there’s the seller incentive problem. 49% of buyers report that sellers won’t even agree to provide post-closing services (Mercer). The ones that do agree aren’t racing to help the buyer leave. Why would they? They’re getting paid.

Technology makes it worse. IT represents over 50% of TSA service costs and takes the longest to exit. Shared ERP systems are the single largest blocker, routinely 12-18 months to separate. When the carved entity’s data lives inside the parent’s SAP instance, “extraction” doesn’t begin to describe the complexity.

And then the cycle starts. The buyer isn’t ready. The TSA gets extended. The extension buys time but kills urgency. Next deadline, same story. Sears and Lands’ End took nearly five years for what was supposed to be a clean separation.

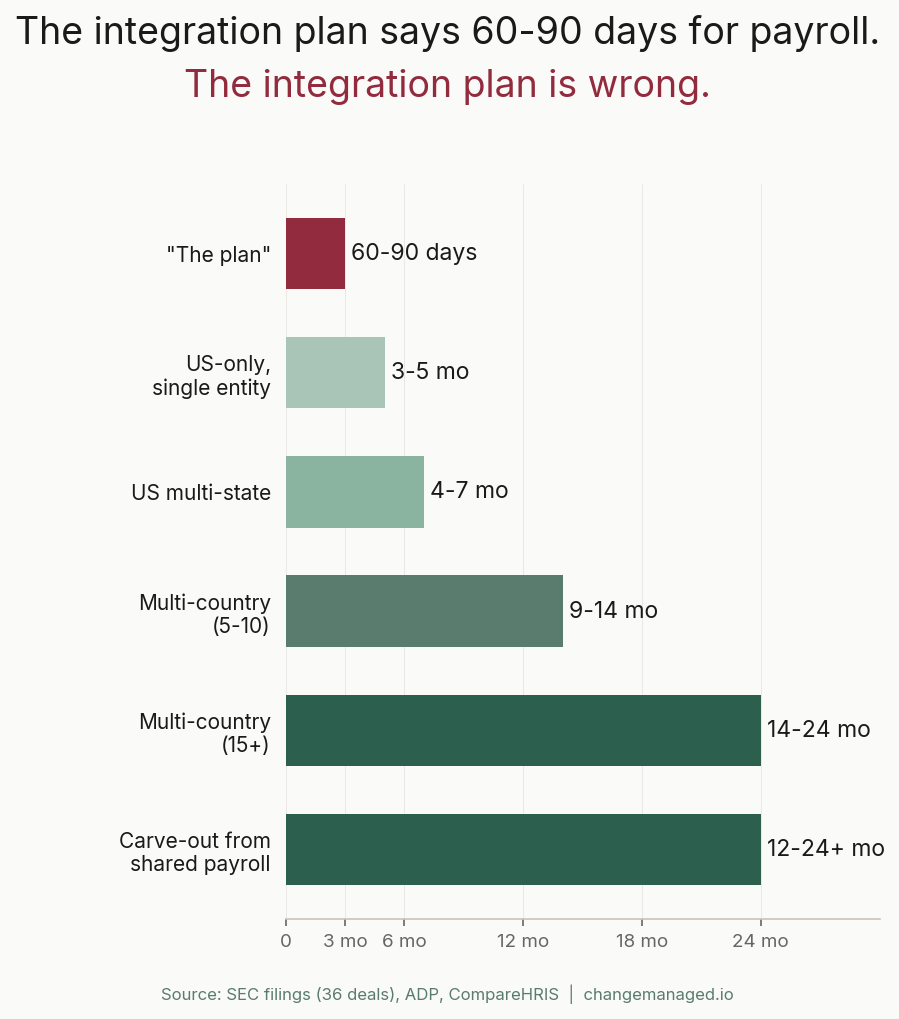

The payroll problem

Payroll is the TSA service line that most teams underestimate the most. It’s also the one where HR integration planning matters most, because payroll failure is visible to every employee on the first pay cycle.

The original plan usually says 60-90 days. That number is wrong for anything beyond the simplest scenario. Even ADP says “90 days minimum” and “closer to six months” for larger organizations. Here’s what’s realistic:

| Scenario | Timeline |

|---|---|

| US-only, single entity | 3-5 months |

| US multi-state | 4-7 months |

| Multi-country (5-10) | 9-14 months |

| Multi-country (15+) | 14-24 months |

| Carve-out from shared payroll | 12-24+ months |

All timelines assume the provider is already selected. Add 2-4 months for the RFP and selection process.

The non-negotiable: parallel payroll runs. Minimum 2 cycles, standard 3, complex or global deals need 4 or more. For monthly payroll, 3 parallel cycles means 3 months of testing alone, on top of all implementation work. CompareHRIS puts it bluntly: “If there isn’t enough time for 2-3 cycles of parallel testing, the go-live date needs to be pushed. Do not shave time from the parallel testing phase.”

This is why the median HR/payroll TSA duration is 18 months. Not because companies want it to take that long. Because it does.

Buyer-side case studies

Most TSA literature is written from the seller’s perspective. Here’s what buyers actually experienced.

Brookfield acquiring Clarios from Johnson Controls ($13.2B, 2019)

Brookfield called the TSA “the lifeblood of a carveout.” The TSA covered payroll, procurement, accounting, IT, and HR for 2 years post-close. Separation costs ran approximately $200M as a one-time charge. Brookfield spent 9 months of negotiations just to receive cost and timeline estimates from JCI.

The strategy: prioritize back-office disentanglement over go-to-market changes. Get standalone before trying to transform.

Result: EBITDA grew from $1.5B to $2.1B. Cash yield hit approximately 23%. Brookfield issued a $4.5B special distribution. The kind of outcome that shows up clearly in a synergy realization tracker.

Danaher acquiring GE Biopharma / Cytiva ($21.4B, 2020)

7,000 employees across 40 countries. The IT separation migrated Oracle EBS from GE’s on-premise infrastructure to Oracle Cloud Infrastructure in 9.5 months, saving $6M+ compared to maintaining GE’s systems.

The lesson: cloud migration during TSA exit can be both faster and cheaper than replicating the parent’s infrastructure.

KKR acquiring Omnissa from Broadcom (~$4B, 2024)

4,000 employees, $1.5B ARR, 26,000 customers. KKR’s team built dedicated sales, services, and support functions before close. IT migration to Omnissa-hosted systems completed in May 2024, ahead of the July close date.

The lesson: building standalone capability pre-close is the single biggest accelerator. Everything that’s done before Day 1 is time that doesn’t need to come from the TSA. I wrote about the full standalone readiness checklist separately.

The cautionary tales

HPE/DXC Technology (2017): Post-close disputes over vague financial definitions led to a $1B lease obligation dispute and a $47.5M class action settlement. When TSA terms are ambiguous, the litigation costs can dwarf the service costs.

Sears/Lands’ End (2014): Vague scope plus no exit discipline equals a multi-year extension trap. What was supposed to be a clean separation took nearly five years. Five years. For Lands’ End. I don’t know what the monthly bill looked like, but I know someone at Sears was very happy about it.

How to actually cut it in half

The biggest single lever is starting before close. Most teams waste 3-6 months post-close just figuring out what they need to build. That’s 3-6 months of TSA duration that adds zero value. Conduct the entanglement analysis during pre-sign. Build standalone capability where you can. KKR had Omnissa’s sales and support functions running before the deal closed. Kellogg invested $80M over 6 years in cloud-first infrastructure that made the eventual separation dramatically faster.

The second lever is sequencing. Not every service line needs 18 months. Exit the easy ones first and concentrate resources on the hard ones:

| Service | Target exit | Approach |

|---|---|---|

| Facilities / Real estate | 30-90 days | Lease new space or negotiate sublease |

| Finance / Accounting | 90-180 days | Stand up GL, AP/AR. Outsource initially if needed. |

| HR / Benefits | 90-180 days | New HRIS. Benefits re-enrollment at plan year boundary. |

| Procurement | 120-180 days | Novate contracts. New vendor relationships. |

| Payroll | 3-14 months | See payroll timelines above. Cannot be compressed. |

| IT / ERP | 6-18 months | Phased extraction. May require greenfield ERP. |

Don’t wait for everything to be ready before exiting anything. Every service line you exit early is one less monthly invoice.

The TSA exit also needs its own program management, separate from the integration PMO. Deloitte recommends a “2-in-a-box” principle: each workstream gets both a seller-side and buyer-side representative. CFO-level sponsors from both organizations. Weekly cadence. Clear owners. Documented decisions. This is not a legal agreement to be managed. It’s a separation to be executed.

Two more things that make a measurable difference. First, make the TSA expensive to keep. Automatic fee escalators after the sunset date (10%+ per month) create urgency on both sides. Pair those with measurable termination criteria (ERP migration complete, payroll system live) so there’s no argument about whether a service has been adequately transitioned. Extensions only by written amendment signed by both CFOs.

Second, consider outsourcing as acceleration. BPO and managed services can bridge the gap between TSA exit and full standalone capability. Outsource payroll to ADP or Ceridian. Use managed IT services while building internal infrastructure. The goal isn’t to build everything yourself. It’s to stop paying the seller.

PE versus corporate playbook

PE buyers and corporate buyers face different TSA dynamics.

PE firms rely more heavily on TSAs because they lack operational infrastructure. There’s no existing HRIS to absorb the carved entity into. No shared services center to extend. Everything must be built or outsourced from scratch.

Bain’s data shows that PE carve-out returns have compressed. Pre-2012: 3.0x MOIC. Post-2012: 1.5x. Top quartile still delivers 2.5x, but the margin for error is smaller. TSA execution has become a key differentiator. The firms that exit TSAs faster capture more of the value creation window.

Corporate buyers have more infrastructure to absorb services quickly, but they often underestimate the entanglement. When you’re absorbing a carved-out division into your existing ERP, the complexity isn’t standing up a new system. It’s merging two data models, two chart-of-accounts structures, and two sets of business rules.

KPMG’s 2026 survey (700 respondents) shows that 57% of corporate dealmakers and 71% of PE firms are pursuing carve-outs. The TSA challenge is only getting bigger.

The pattern that works

Every fast TSA exit I’ve seen or studied shares three traits. The team started separation work before close. They sequenced service exits instead of trying to move everything at once. And they treated the TSA as a countdown, not a safety net.

The Kellanova/WK Kellogg separation is the best public example. Seven workstreams. 300+ systems. $80M in standalone investment. But the real story is what happened before the separation was announced: 6 years of cloud-first migration, 2,500+ servers already moved, and a data rationalization that found only about 150 of “thousands of reports” were actually used. The rest were artifacts nobody needed.

Most companies won’t have 6 years of preparation. You probably don’t. But every week of standalone readiness work done before the TSA clock starts is a week you don’t need from the seller. That math doesn’t change regardless of deal size. For a practical 100-day roadmap that puts TSA exit in the broader integration context, start there.

Related Reading

- Carve-Out Readiness: What to Build Before Day 1

- HR Integration in M&A: The Playbook That Should Exist

- How to Set Up an IMO That Actually Works

- M&A Retention Bonuses: The ROI Math Nobody Shows You

If your TSA is running longer than planned and the extension bills keep coming, let’s talk. The exit plan should have started before close. It’s not too late to build one now.

Related Insights

Carve-Out Readiness Checklist: 23 Items Before Day 1

The priority-tiered carve-out checklist. What must work Day 1, what starts before close, and what can wait. HRIS, payroll, legal entities, compliance, ERP.

100-Day M&A Integration Plan

100-day post-merger integration plan: stabilize (0-30), execute (31-60), accelerate (61-100). Week-by-week milestones from real transactions.

Josh is a Roshco founder. 15+ years leading M&A integrations, org redesigns, and technology transformations across multiple multi-billion-dollar deals and carve-outs. Deloitte Human Capital alum. UPenn. Prosci certified. Navy veteran.

See it in action

Orgscout puts live deal intelligence behind the advisory work: dashboards, org design, and synergy tracking on real data.

Explore the platform